Open access fiber

New investment opportunities opening up for gigabit broadband in Europe

Executive Summary

Fiber and open access fiber deal activity has been high in 2019, accounting for 45 percent of total telecom sector deal value, suggesting a high interest from investors, including from traditionally non-telco investors like infrastructure funds, energy companies and so forth. Investing in open access fiber is an ecosystem game changer, not just because it delivers macroeconomic benefits to the country but because it brings in higher valuations to shareholders (compared to traditional integrated telecom entities), delivers better operational efficiency KPIs to telecom operators and provides better customer experience to end users.

We have observed some common themes in successful open access fiber business models. First, they involve multi-party investment from several entities outside the telecom ecosystem, such as energy companies, municipalities, real estate companies and infrastructure investors. These entities bring in not only fresh capital but also expertise to roll out and operate long-term infrastructure, like fiber. Second, commercialization success is catalyzed by open access wholesale models because almost all retail telcos have access to the same underlying wholesale fiber infrastructure, accelerating take-up and improving overall operational economics.

As open access fiber gains acceptance, traditional telecom operators are adjusting their fixed broadband strategies accordingly. Traditionally, incumbents resisted partnering with open access fiber entities and fought against doing so by accelerating their own fiber (fiber to the home [FTTH] or fiber to the curb [FTTC]) rollout. Recently, however, we have seen some incumbents trying to partner (through wholesale and whole-buy agreements) or acquire open access fiber entities. In addition, cable companies are trying to avoid getting squeezed out by incumbents on one side and open access fiber challengers on the other side by making incremental upgrades to their cable networks or by tactically reselling wholesale fiber when possible. Meanwhile, challenger telcos are proactively forging partnerships with open access fiber entities and are aggressively trying to expand their fixed broadband offerings to gain market share in what was traditionally the incumbents’ turf. Non-telcos, especially energy and utility companies, are seeing new business opportunities in open access fiber in selected markets to both invest as well as operate fiber infrastructure.

We believe open access fiber will continue to expand, especially in markets that do not yet have nationwide fiber access. If the deal volume in 2020 is similar to the deal volume in 2019, we can expect enough funding for 24 million new homes to be passed with fiber this year.

1

High activity in open access fiber deals in Europe in 2018-19

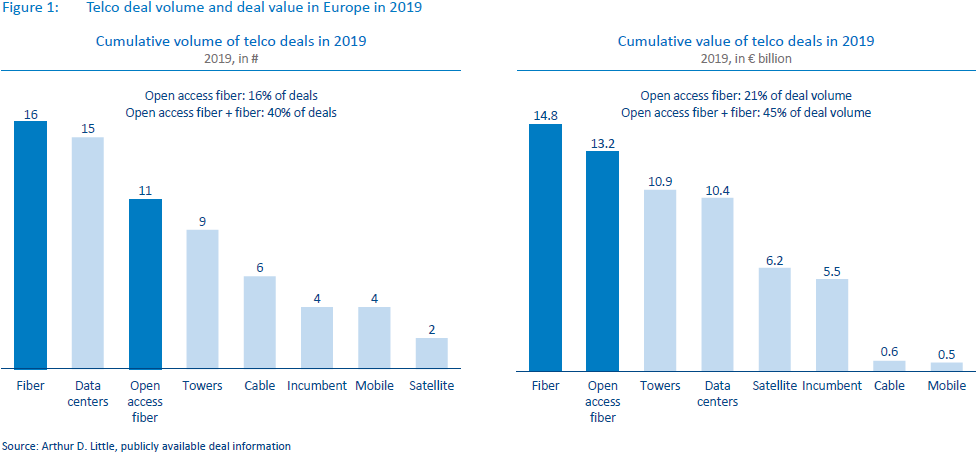

Europe saw approximately 60€ billion worth of telecom sector deals in 2019, of which fiber and open access fiber transactions together contributed a share of 45 percent (see Figure 1). More than half the fiber deals executed last year were open access fiber, with a total value of 13.2€ billion, the largest of them coming from Deutsche Glasfaser DE, inexio DE, Covage FR, Altice PT, CityFibre UK, in addition to the Open Fiber IT deal in 2018. All top five EU countries have witnessed at least one highprofile open access fiber transaction in the last two years.

Open access fiber together with fiber is clearly taking the lead in almost all telco deals, with fresh external investment coming from private equity (PE) funds/infrastructure funds (e.g., Deutsche Glasfaser, inexio) and energy companies (Open Fiber), in addition to government funding for rural fiber and traditional telecom investment in fiber. (We provide a detailed perspective into the origins of FTTH wholesaling, giving rise to a case for a new fiber model, in our upcoming Arthur D. Little report, “A new future to come: M&A delivering ideas on FTTH wholesaling. ”)

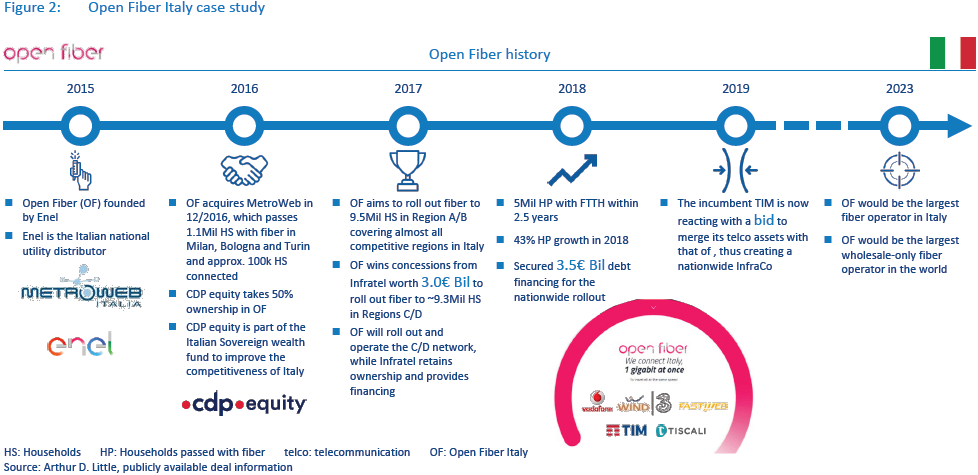

The most prominent of all these deals comes from Open Fiber, which announced nationwide fiber coverage for Italy, with a business plan to pass 18 million homes over the next six years (see Figure 2). Subsequently, the company has successfully obtained 3€ billion in government funding for rural fiber and another 3.5€ billion of debt funding for the rest of the country. In the first quarter of 2020, Bloomberg reported that Open Fiber might become a target of a high-profile acquisition by the incumbent Telecomm Italia (TIM), along with PE fund KKR, to create a nationwide open access fixed infrastructure provider in Italy. It is noteworthy that Italy, which until recently was one of the lagging fiber markets, is now seeing multi-billion-dollar interest – not just from Open Fiber but also from TIM. These deals are expected to propel Italy as one of the leading fiber markets in Europe in the next five years.

2

Investing in open access fiber is an ecosystem game changer

Investing in open access fiber is not a business-as-usual strategy, but rather an ecosystem game changer for the whole country. The impact on the macroeconomic fundamentals of the market is significant, with the economy, investors, operators and end users standing to benefit in the following ways:

- Macroeconomic benefit to the country.

- Higher valuations/returns to shareholders.

- Better efficiency and commercialization success to operators.

- Gigabit speeds at affordable prices.

Macroeconomic benefit to the country

- Open access fiber pushes fiber coverage across the whole country above 80 percent. Especially in markets where ultrahigh- speed broadband penetration has been stagnating for many years below 20 percent (e.g., in Italy and Germany), the impact of open access fiber is significant. Given that fiber is necessary for future 5G rollout and to accelerate digitalization in the market, the benefit of fiber outside the telecom sector is further amplified.

- The COVID-19 crisis has further emphasized that access to high-speed broadband is necessary for a successful digital ecosystem. A detailed analysis of the impact of COVID-19 on the telecom sector, as well as the economy in general, is covered in a special report published by Arthur D. Little.

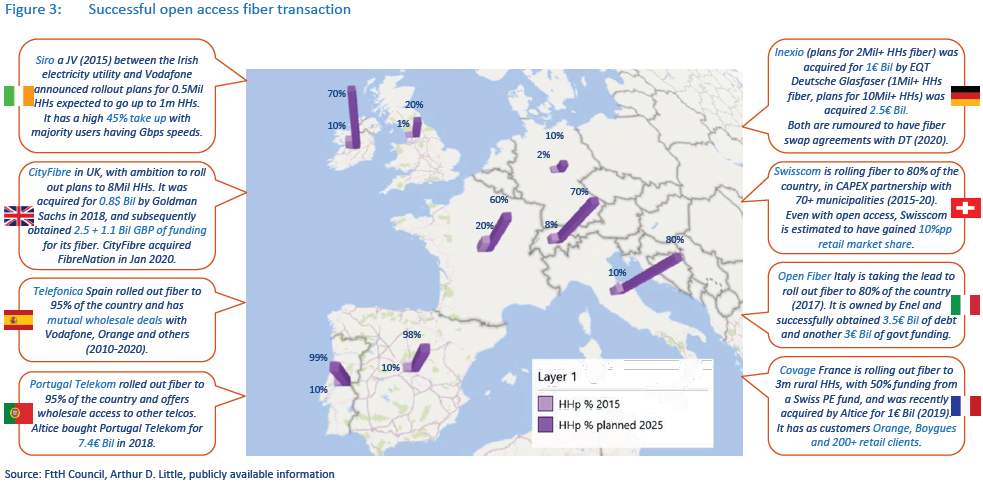

- Open access fiber encourages new investments from traditionally non-telecom players in the telecom sector. Entities such as PE funds, infrastructure funds, debt lenders and so on, are taking an active interest to invest in open access fiber ventures. Typically, up to 80 percent funding can be obtained from such third-party non-telco entities, bringing in fresh capital to the telecom industry and providing much needed funding relief to the telecom sector. Consider the case of Open Fiber, which obtained more than 3€ billion of funding from the government and another 3.5€ billion from a consortium of multiple banks, while the equity investment is estimated to have been less than 1€ billion. This is an effective example of fresh capital injection into the telecom sector. In Figure 3, we highlight successful fiber transactions in the recent years that either raised capital through infrastructure funds or forged successful wholesale/wholebuy agreements with other telco entities.

Higher valuations/returns to shareholders

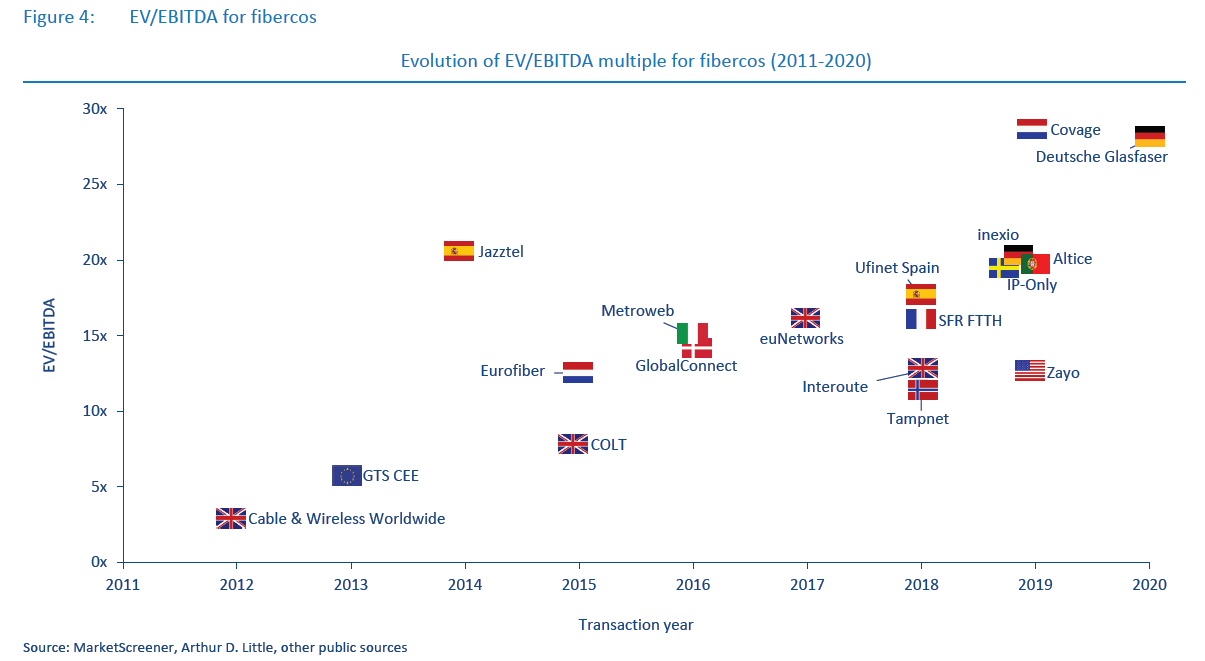

- Open access fiber companies have demonstrated higher valuations versus traditional telco players – sometimes recent transactions have been estimated as high as 10-25x EBITDA versus 5-8x for traditional telcos. A reason for the high valuations could be that open access fiber is a longterm, low-OPEX, stable asset backed up with multiple longterm wholesale contracts, which in theory is more similar to infrastructure businesses (e.g., energy, transportation) than telecom. Such potentially high valuations are encouraging shareholders of some incumbent telcos to consider carving out and spinning off their infrastructure into an independent entity to invest in fiber or merging with an existing fiber entity.

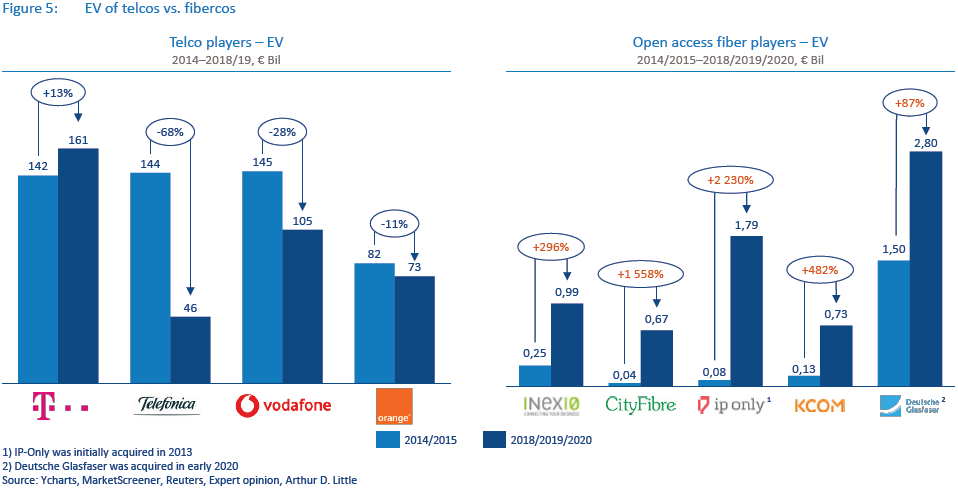

- Open access fiber entities have shown substantial value creation in terms of enterprise value (EV) increase in the last five years (as seen in Figure 4), sometimes as high as a 10x value increase, compared to EV erosion in four of the largest European telcos (as seen in Figure 5).

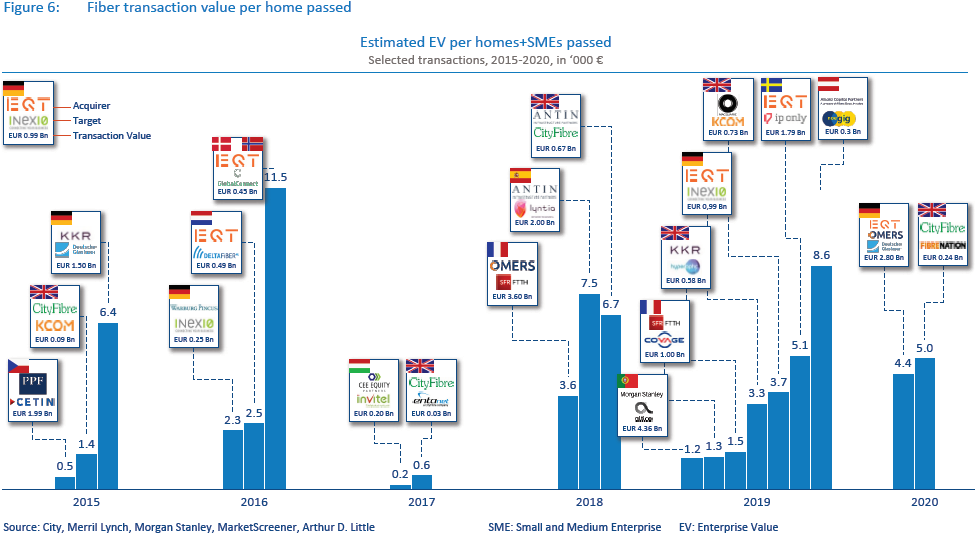

- Open access fiber entities have shown consistent increases in transaction value per home passed in the last five years, from an average of 5x in 2015 to 5-10x in 2018-19.

- In Figure 6, we plot the estimated EV based on publicly available information about the number of homes passed with fiber during the time of the deal. Note that most fiber entities have a large amount of debt; hence the actual equity value of the transaction and the cash that the acquirer pays the target is usually lower by a factor of 3-5x than the EV indicated in the figure. Moreover, many of these deals happened during the early life of the fiberco, indicating that potential acquirers are willing to pay a premium for the future coverage that the fiberco hopes to achieve.

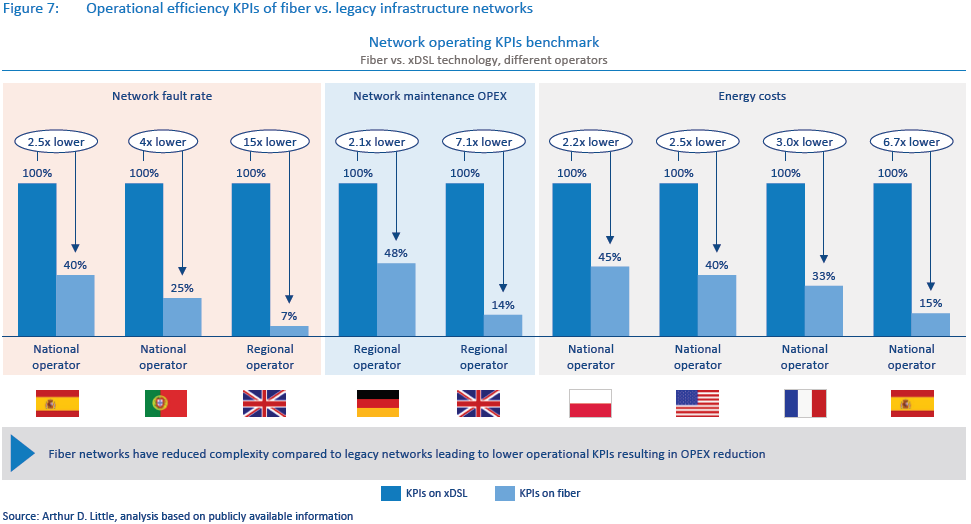

- Open access fiber is operationally more efficient compared to incumbent legacy networks, sometimes by a factor of 2-7x, as optical networks are inherently easier to operate than traditional copper-based networks (as shown in Figure 7). This results in much lower operational costs, along with better margins compared to legacy fixed networks.

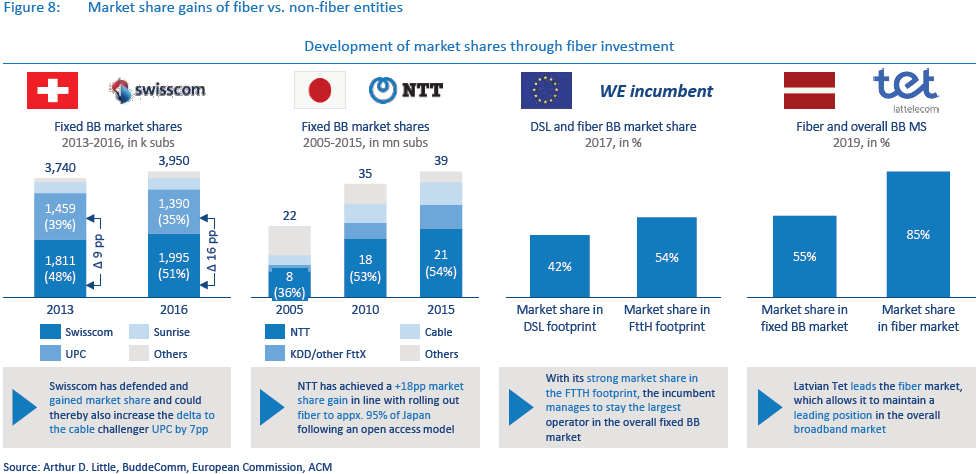

- Fiber operators achieve market share gains from non-fiber operators, and even from existing cable operators. Telcos with open access fiber have gained up to 5pp (percentage points) of market share, even though they provide open access fiber to competitors (as illustrated in Figure 8). For example, Swisscom in Switzerland is reported to have increased its market share by 6pp even though it has supplied all its competitors with open access fiber in the last five years. When fiber is available in the market to all players, the focus of competition shifts from providing merely higher broadband speeds to providing higher-quality customer experience and new services.

- Fiber operators typically have 5-10pp lower churn compared to non-fiber players. This is the highest-impacting business driver for telcos pushing fiber broadband versus legacy, and even versus cable broadband.

Gigabit speeds at affordable prices

- Open access fiber democratizes gigabit broadband – In markets with open access fiber, such as Singapore and Italy, gigabit-speed packages are considered the base packages that are offered to customers at affordable prices of 25-30€/ month. In markets with availability of wholesale fiber, such as Spain and Portugal, gigabit speeds are common (although not always the base package), and prices are in the range of 40-60€/month. In markets with exclusive fiber operators, such as UAE and Qatar, gigabit-speed offers are considered premium packages and are priced at a rate of 300-600€/ month. This observation leads us to conclude that availability of open access fiber or even wholesale fiber democratizes gigabit broadband access in terms of high-speed availability and affordable monthly prices.

- Fiber-based broadband provides better customer experience to the end user. The value proposition is not just high speeds, but also the increased quality of services the customer perceives while using broadband. It gives the telCo an opportunity to up-sell new partner content, such as streaming services, etc. Many of the gigabit speed bundles (as seen in Figure 9) also have bundled TV and other OTT (“over the top”) content.

3

Success factors observed in open access fiber business models

We have observed some recurring success factors in recent open access fiber business models:

- Obtaining multi-party investment, not only from telco players but also from non-telco players, such as energy companies, infrastructure funds, etc. As we mentioned earlier in this report, non-telco entities invested multi-billion euros in open access fiber transactions in Europe in 2019; we expect this trend to continue into 2020 and beyond.

- Leveraging expertise of entities outside the telecom ecosystem for efficiently rolling out fiber. Typically, energy companies, municipalities, real estate companies, etc., have more expertise than traditional telecom companies in rolling out fiber, including skills such as project management across multiple entities, resolving local bureaucratic hurdles, ramping up staff and redeploying staff from one region to another. Open access fiber operators also tend to use new technology-enabled tools such as autonomous cars that drive around a targeted region collecting GIS data to assist in rollout planning and demand aggregation, with inputs from multiple telcos to identify the best areas to roll out, ultimately leading to timely rollout at lower unit costs.

- Ensuring high fiber uptake by signing up all key players in the market as wholesale customers. This implies that all key retail telco players (in some cases, even the incumbents) sign up with long-term contracts to use wholesale fiber. In the best case, the retail companies also announce that they would stop rolling out their own competing/overlapping fiber with the open access fiber company (as Vodafone Italy announced in 2018 after its wholesale deal with Open Fiber).

4

Strategies pursued by telcos in reaction to increased interest in open access fiber

Incumbents attempt to maintain or retake the lead

We have observed incumbents attempting to maintain or retake the lead in shaping the fiber roadmaps for their respective countries (as seen in Figure 10). Although incumbents have traditionally resisted partnering with other entities or opening their fiber networks for wholesale services, we see some incumbents warming to the idea of taking a role in establishing open access fiber infrastructure.

There have been rumors of strategic moves by multiple incumbents in Europe in this direction, and we believe many new fiber deals will be announced soon by incumbents in Europe that are either partnering directly with challenger open access fiber entities or are partnering with other nontelco entities to roll out large-scale open access fiber in their respective countries. (An upcoming Arthur D. Little report will provide further details on incumbent fiber strategies.)

Shutting down the legacy copper network is another strategic advantage of rolling out a nationwide fiber network, which we assess in detail in Arthur D. Little’s upcoming edition of “Race to Gigabit Fiber 2020.”

Cable companies avoid getting squeezed by incumbents on one side and open access fiber challengers on the other side

Cable companies historically have benefited from superior data speeds as well as low churn rates of their subscribers compared to other fixed broadband products like xDSL. But with gigabit FTTH, cablecos are now increasingly being challenged on multiple fronts.

Cablecos usually sell their services using their own retail brand, while open access fiber operators resell services to multiple telcos, giving telcos a much higher chance of achieving higher utilization of their fiber network. This increased utilization leads to overall better economics compared to cablecos’ cable networks.

Typical cable networks consist of multiple active components, which inherently require higher operations/maintenance and energy costs versus fiber networks, which have a higher share of passive components that are easier to operate. Consequently, cable networks eventually succumb to cost disadvantage when competing with fiber-only networks. Additionally, to deliver gigabit speeds to customers, cablecos have to plan for a new wave of CAPEX to upgrade their infrastructure to Docsis 4.0, whereas FTTH networks can already deliver gigabit speeds and symmetric speeds.

Moreover, the use of videoconferencing, real-time collaboration tools and cloud-based services is constantly on the rise, implying that not just high speeds but also symmetric connectivity with low latency are required. The recent COVID-19 crisis has given a strong impetus for the use of these tools, and we believe the adoption of remote working tools will continue to increase after the pandemic. Fiber networks have a better performance compared to cable networks when it comes to symmetric high speeds with low latency.

Given the above challenges cablecos face, and with increasing fiber rollout by competitors, cablecos are also directly or indirectly obtaining access to fiber. Some cable companies, such as Vodafone, are tactically extending their footprint with wholebuy agreements with other open access fiber providers, such as Deutsche Glasfaser. In another example, StarHub SG is using the open access fiber available in Singapore for its customers and is reported to have decommissioned its cable network in 2019.

Challenger telcos proactively forge partnerships or whole-buy agreements with open access fiber entities

We are seeing challenger telcos increasingly cooperate with open access fiber entities as they seek to benefit from wholesale access to gigabit broadband networks. Theoretically, the greater the number of telcos signing up with long-term wholesale contracts with open access fiber providers, the higher the probability of success of low-cost rollout and higher gigabit broadband penetration in that market.

In Italy, for example, Open Fiber signed whole-buy agreements with almost all challenger telco operators in the first years of its launch, enabling it to scale up its business from a regional provider focusing on a few regions in northern Italy to a national entity with nationwide rollout plans. Such large-scale scale-up is not without operational, financial and political challenges. Thus, we are observing with keen interest the fiber market developments in Italy.

As another example, Vodafone has used a mix of all the above strategies to improve its access to gigabit fixed infrastructure. In Germany, Vodafone DE followed the M&A route to gain a strong foothold in the fixed infrastructure market with its acquisition of Kabel Deutschland seven years ago. Vodafone DE is continuing to expand its footprint with whole-buy agreements with Deutsche Glasfaser, inexio and other regional fiber network providers in Germany. In Italy, Vodafone IT was previously investing in building its own FTTC network. However, after its deal with Open Fiber in 2017-18, Vodafone IT announced a stop to all future FTTC investment, relying exclusively on Open Fiber’s FTTH network for nationwide coverage. In the UK, Vodafone UK has struck multiple agreements with Openreach, CityFibre and others to expand its fiber footprint. In Ireland, Vodafone co-invested, along with the electric company ESB in SIRO to roll out open access fiber.

New opportunities for non-telco companies

Open access fiber is opening up new opportunities for nontelco companies, like energy companies, municipalities, infrastructure funds and others, to invest in future nationwide critical infrastructure – often with positive government support. Although the quantum of investment is large, open access fiber offers long-term stable cash flows and higher multiples, thus offering an attractive alternative to traditional telecom equity or debt investment. Italian utility Enel, through its investment in Open Fiber; ESB in SIRO Ireland; DeltaFiber in the Netherlands and Germany; KKR in Deutsche Glasfaser, etc., have all seen high valuations, as illustrated earlier in Figure 6. Non-telco firms are also taking active interest in owning parts of the fiber network, as seen in the interest in the ongoing Bouygues fiber transactions of two sub-projects in France.

Conclusion

We believe open access fiber will continue to gain steam and fresh investment will pour into this market in the coming years. Incumbents, cable companies, challenger telcos and non-telco entities like energy companies, municipalities and PE/infrastructure funds all have key roles to play in building sustainable nationwide gigabit fiber in their respective markets. Proactive moves from some Telcos like Vodafone DE or nontelcos like Open Fiber have placed them in a leading position in shaping the gigabit future of their markets. Incumbent telcos have made and are continuing to make big moves, as rumored in Italy and a few other European markets.

If we assume that the deal volume in 2020 will be approximately 60€ billion (similar to the volume in 2019) and assume a similar 40 percent of share of fiber or open access fiber in the total deal volume, we predict funding of 24€ billion going into the fiber sector in Europe. Assuming an average of 1000€ CAPEX required to pass a home with fiber, this implies 24 million new homes can be passed with fiber in 2020 alone. To put this in perspective, the whole of the UK or France can be passed with fiber in just one year. As availability of open access fiber increases, we will see a proliferation of multi-gigabit offers in the market delivered over FTTH, as we have already seen in Singapore and which are also occurring in Italy, Spain and Portugal, among others.

We will continue to watch with interest and report on the developments in this space in the future.

DOWNLOAD THE FULL REPORT

Open access fiber

New investment opportunities opening up for gigabit broadband in Europe

DATE

Executive Summary

Fiber and open access fiber deal activity has been high in 2019, accounting for 45 percent of total telecom sector deal value, suggesting a high interest from investors, including from traditionally non-telco investors like infrastructure funds, energy companies and so forth. Investing in open access fiber is an ecosystem game changer, not just because it delivers macroeconomic benefits to the country but because it brings in higher valuations to shareholders (compared to traditional integrated telecom entities), delivers better operational efficiency KPIs to telecom operators and provides better customer experience to end users.

We have observed some common themes in successful open access fiber business models. First, they involve multi-party investment from several entities outside the telecom ecosystem, such as energy companies, municipalities, real estate companies and infrastructure investors. These entities bring in not only fresh capital but also expertise to roll out and operate long-term infrastructure, like fiber. Second, commercialization success is catalyzed by open access wholesale models because almost all retail telcos have access to the same underlying wholesale fiber infrastructure, accelerating take-up and improving overall operational economics.

As open access fiber gains acceptance, traditional telecom operators are adjusting their fixed broadband strategies accordingly. Traditionally, incumbents resisted partnering with open access fiber entities and fought against doing so by accelerating their own fiber (fiber to the home [FTTH] or fiber to the curb [FTTC]) rollout. Recently, however, we have seen some incumbents trying to partner (through wholesale and whole-buy agreements) or acquire open access fiber entities. In addition, cable companies are trying to avoid getting squeezed out by incumbents on one side and open access fiber challengers on the other side by making incremental upgrades to their cable networks or by tactically reselling wholesale fiber when possible. Meanwhile, challenger telcos are proactively forging partnerships with open access fiber entities and are aggressively trying to expand their fixed broadband offerings to gain market share in what was traditionally the incumbents’ turf. Non-telcos, especially energy and utility companies, are seeing new business opportunities in open access fiber in selected markets to both invest as well as operate fiber infrastructure.

We believe open access fiber will continue to expand, especially in markets that do not yet have nationwide fiber access. If the deal volume in 2020 is similar to the deal volume in 2019, we can expect enough funding for 24 million new homes to be passed with fiber this year.

1

High activity in open access fiber deals in Europe in 2018-19

Europe saw approximately 60€ billion worth of telecom sector deals in 2019, of which fiber and open access fiber transactions together contributed a share of 45 percent (see Figure 1). More than half the fiber deals executed last year were open access fiber, with a total value of 13.2€ billion, the largest of them coming from Deutsche Glasfaser DE, inexio DE, Covage FR, Altice PT, CityFibre UK, in addition to the Open Fiber IT deal in 2018. All top five EU countries have witnessed at least one highprofile open access fiber transaction in the last two years.

Open access fiber together with fiber is clearly taking the lead in almost all telco deals, with fresh external investment coming from private equity (PE) funds/infrastructure funds (e.g., Deutsche Glasfaser, inexio) and energy companies (Open Fiber), in addition to government funding for rural fiber and traditional telecom investment in fiber. (We provide a detailed perspective into the origins of FTTH wholesaling, giving rise to a case for a new fiber model, in our upcoming Arthur D. Little report, “A new future to come: M&A delivering ideas on FTTH wholesaling. ”)

The most prominent of all these deals comes from Open Fiber, which announced nationwide fiber coverage for Italy, with a business plan to pass 18 million homes over the next six years (see Figure 2). Subsequently, the company has successfully obtained 3€ billion in government funding for rural fiber and another 3.5€ billion of debt funding for the rest of the country. In the first quarter of 2020, Bloomberg reported that Open Fiber might become a target of a high-profile acquisition by the incumbent Telecomm Italia (TIM), along with PE fund KKR, to create a nationwide open access fixed infrastructure provider in Italy. It is noteworthy that Italy, which until recently was one of the lagging fiber markets, is now seeing multi-billion-dollar interest – not just from Open Fiber but also from TIM. These deals are expected to propel Italy as one of the leading fiber markets in Europe in the next five years.

2

Investing in open access fiber is an ecosystem game changer

Investing in open access fiber is not a business-as-usual strategy, but rather an ecosystem game changer for the whole country. The impact on the macroeconomic fundamentals of the market is significant, with the economy, investors, operators and end users standing to benefit in the following ways:

- Macroeconomic benefit to the country.

- Higher valuations/returns to shareholders.

- Better efficiency and commercialization success to operators.

- Gigabit speeds at affordable prices.

Macroeconomic benefit to the country

- Open access fiber pushes fiber coverage across the whole country above 80 percent. Especially in markets where ultrahigh- speed broadband penetration has been stagnating for many years below 20 percent (e.g., in Italy and Germany), the impact of open access fiber is significant. Given that fiber is necessary for future 5G rollout and to accelerate digitalization in the market, the benefit of fiber outside the telecom sector is further amplified.

- The COVID-19 crisis has further emphasized that access to high-speed broadband is necessary for a successful digital ecosystem. A detailed analysis of the impact of COVID-19 on the telecom sector, as well as the economy in general, is covered in a special report published by Arthur D. Little.

- Open access fiber encourages new investments from traditionally non-telecom players in the telecom sector. Entities such as PE funds, infrastructure funds, debt lenders and so on, are taking an active interest to invest in open access fiber ventures. Typically, up to 80 percent funding can be obtained from such third-party non-telco entities, bringing in fresh capital to the telecom industry and providing much needed funding relief to the telecom sector. Consider the case of Open Fiber, which obtained more than 3€ billion of funding from the government and another 3.5€ billion from a consortium of multiple banks, while the equity investment is estimated to have been less than 1€ billion. This is an effective example of fresh capital injection into the telecom sector. In Figure 3, we highlight successful fiber transactions in the recent years that either raised capital through infrastructure funds or forged successful wholesale/wholebuy agreements with other telco entities.

Higher valuations/returns to shareholders

- Open access fiber companies have demonstrated higher valuations versus traditional telco players – sometimes recent transactions have been estimated as high as 10-25x EBITDA versus 5-8x for traditional telcos. A reason for the high valuations could be that open access fiber is a longterm, low-OPEX, stable asset backed up with multiple longterm wholesale contracts, which in theory is more similar to infrastructure businesses (e.g., energy, transportation) than telecom. Such potentially high valuations are encouraging shareholders of some incumbent telcos to consider carving out and spinning off their infrastructure into an independent entity to invest in fiber or merging with an existing fiber entity.

- Open access fiber entities have shown substantial value creation in terms of enterprise value (EV) increase in the last five years (as seen in Figure 4), sometimes as high as a 10x value increase, compared to EV erosion in four of the largest European telcos (as seen in Figure 5).

- Open access fiber entities have shown consistent increases in transaction value per home passed in the last five years, from an average of 5x in 2015 to 5-10x in 2018-19.

- In Figure 6, we plot the estimated EV based on publicly available information about the number of homes passed with fiber during the time of the deal. Note that most fiber entities have a large amount of debt; hence the actual equity value of the transaction and the cash that the acquirer pays the target is usually lower by a factor of 3-5x than the EV indicated in the figure. Moreover, many of these deals happened during the early life of the fiberco, indicating that potential acquirers are willing to pay a premium for the future coverage that the fiberco hopes to achieve.

- Open access fiber is operationally more efficient compared to incumbent legacy networks, sometimes by a factor of 2-7x, as optical networks are inherently easier to operate than traditional copper-based networks (as shown in Figure 7). This results in much lower operational costs, along with better margins compared to legacy fixed networks.

- Fiber operators achieve market share gains from non-fiber operators, and even from existing cable operators. Telcos with open access fiber have gained up to 5pp (percentage points) of market share, even though they provide open access fiber to competitors (as illustrated in Figure 8). For example, Swisscom in Switzerland is reported to have increased its market share by 6pp even though it has supplied all its competitors with open access fiber in the last five years. When fiber is available in the market to all players, the focus of competition shifts from providing merely higher broadband speeds to providing higher-quality customer experience and new services.

- Fiber operators typically have 5-10pp lower churn compared to non-fiber players. This is the highest-impacting business driver for telcos pushing fiber broadband versus legacy, and even versus cable broadband.

Gigabit speeds at affordable prices

- Open access fiber democratizes gigabit broadband – In markets with open access fiber, such as Singapore and Italy, gigabit-speed packages are considered the base packages that are offered to customers at affordable prices of 25-30€/ month. In markets with availability of wholesale fiber, such as Spain and Portugal, gigabit speeds are common (although not always the base package), and prices are in the range of 40-60€/month. In markets with exclusive fiber operators, such as UAE and Qatar, gigabit-speed offers are considered premium packages and are priced at a rate of 300-600€/ month. This observation leads us to conclude that availability of open access fiber or even wholesale fiber democratizes gigabit broadband access in terms of high-speed availability and affordable monthly prices.

- Fiber-based broadband provides better customer experience to the end user. The value proposition is not just high speeds, but also the increased quality of services the customer perceives while using broadband. It gives the telCo an opportunity to up-sell new partner content, such as streaming services, etc. Many of the gigabit speed bundles (as seen in Figure 9) also have bundled TV and other OTT (“over the top”) content.

3

Success factors observed in open access fiber business models

We have observed some recurring success factors in recent open access fiber business models:

- Obtaining multi-party investment, not only from telco players but also from non-telco players, such as energy companies, infrastructure funds, etc. As we mentioned earlier in this report, non-telco entities invested multi-billion euros in open access fiber transactions in Europe in 2019; we expect this trend to continue into 2020 and beyond.

- Leveraging expertise of entities outside the telecom ecosystem for efficiently rolling out fiber. Typically, energy companies, municipalities, real estate companies, etc., have more expertise than traditional telecom companies in rolling out fiber, including skills such as project management across multiple entities, resolving local bureaucratic hurdles, ramping up staff and redeploying staff from one region to another. Open access fiber operators also tend to use new technology-enabled tools such as autonomous cars that drive around a targeted region collecting GIS data to assist in rollout planning and demand aggregation, with inputs from multiple telcos to identify the best areas to roll out, ultimately leading to timely rollout at lower unit costs.

- Ensuring high fiber uptake by signing up all key players in the market as wholesale customers. This implies that all key retail telco players (in some cases, even the incumbents) sign up with long-term contracts to use wholesale fiber. In the best case, the retail companies also announce that they would stop rolling out their own competing/overlapping fiber with the open access fiber company (as Vodafone Italy announced in 2018 after its wholesale deal with Open Fiber).

4

Strategies pursued by telcos in reaction to increased interest in open access fiber

Incumbents attempt to maintain or retake the lead

We have observed incumbents attempting to maintain or retake the lead in shaping the fiber roadmaps for their respective countries (as seen in Figure 10). Although incumbents have traditionally resisted partnering with other entities or opening their fiber networks for wholesale services, we see some incumbents warming to the idea of taking a role in establishing open access fiber infrastructure.

There have been rumors of strategic moves by multiple incumbents in Europe in this direction, and we believe many new fiber deals will be announced soon by incumbents in Europe that are either partnering directly with challenger open access fiber entities or are partnering with other nontelco entities to roll out large-scale open access fiber in their respective countries. (An upcoming Arthur D. Little report will provide further details on incumbent fiber strategies.)

Shutting down the legacy copper network is another strategic advantage of rolling out a nationwide fiber network, which we assess in detail in Arthur D. Little’s upcoming edition of “Race to Gigabit Fiber 2020.”

Cable companies avoid getting squeezed by incumbents on one side and open access fiber challengers on the other side

Cable companies historically have benefited from superior data speeds as well as low churn rates of their subscribers compared to other fixed broadband products like xDSL. But with gigabit FTTH, cablecos are now increasingly being challenged on multiple fronts.

Cablecos usually sell their services using their own retail brand, while open access fiber operators resell services to multiple telcos, giving telcos a much higher chance of achieving higher utilization of their fiber network. This increased utilization leads to overall better economics compared to cablecos’ cable networks.

Typical cable networks consist of multiple active components, which inherently require higher operations/maintenance and energy costs versus fiber networks, which have a higher share of passive components that are easier to operate. Consequently, cable networks eventually succumb to cost disadvantage when competing with fiber-only networks. Additionally, to deliver gigabit speeds to customers, cablecos have to plan for a new wave of CAPEX to upgrade their infrastructure to Docsis 4.0, whereas FTTH networks can already deliver gigabit speeds and symmetric speeds.

Moreover, the use of videoconferencing, real-time collaboration tools and cloud-based services is constantly on the rise, implying that not just high speeds but also symmetric connectivity with low latency are required. The recent COVID-19 crisis has given a strong impetus for the use of these tools, and we believe the adoption of remote working tools will continue to increase after the pandemic. Fiber networks have a better performance compared to cable networks when it comes to symmetric high speeds with low latency.

Given the above challenges cablecos face, and with increasing fiber rollout by competitors, cablecos are also directly or indirectly obtaining access to fiber. Some cable companies, such as Vodafone, are tactically extending their footprint with wholebuy agreements with other open access fiber providers, such as Deutsche Glasfaser. In another example, StarHub SG is using the open access fiber available in Singapore for its customers and is reported to have decommissioned its cable network in 2019.

Challenger telcos proactively forge partnerships or whole-buy agreements with open access fiber entities

We are seeing challenger telcos increasingly cooperate with open access fiber entities as they seek to benefit from wholesale access to gigabit broadband networks. Theoretically, the greater the number of telcos signing up with long-term wholesale contracts with open access fiber providers, the higher the probability of success of low-cost rollout and higher gigabit broadband penetration in that market.

In Italy, for example, Open Fiber signed whole-buy agreements with almost all challenger telco operators in the first years of its launch, enabling it to scale up its business from a regional provider focusing on a few regions in northern Italy to a national entity with nationwide rollout plans. Such large-scale scale-up is not without operational, financial and political challenges. Thus, we are observing with keen interest the fiber market developments in Italy.

As another example, Vodafone has used a mix of all the above strategies to improve its access to gigabit fixed infrastructure. In Germany, Vodafone DE followed the M&A route to gain a strong foothold in the fixed infrastructure market with its acquisition of Kabel Deutschland seven years ago. Vodafone DE is continuing to expand its footprint with whole-buy agreements with Deutsche Glasfaser, inexio and other regional fiber network providers in Germany. In Italy, Vodafone IT was previously investing in building its own FTTC network. However, after its deal with Open Fiber in 2017-18, Vodafone IT announced a stop to all future FTTC investment, relying exclusively on Open Fiber’s FTTH network for nationwide coverage. In the UK, Vodafone UK has struck multiple agreements with Openreach, CityFibre and others to expand its fiber footprint. In Ireland, Vodafone co-invested, along with the electric company ESB in SIRO to roll out open access fiber.

New opportunities for non-telco companies

Open access fiber is opening up new opportunities for nontelco companies, like energy companies, municipalities, infrastructure funds and others, to invest in future nationwide critical infrastructure – often with positive government support. Although the quantum of investment is large, open access fiber offers long-term stable cash flows and higher multiples, thus offering an attractive alternative to traditional telecom equity or debt investment. Italian utility Enel, through its investment in Open Fiber; ESB in SIRO Ireland; DeltaFiber in the Netherlands and Germany; KKR in Deutsche Glasfaser, etc., have all seen high valuations, as illustrated earlier in Figure 6. Non-telco firms are also taking active interest in owning parts of the fiber network, as seen in the interest in the ongoing Bouygues fiber transactions of two sub-projects in France.

Conclusion

We believe open access fiber will continue to gain steam and fresh investment will pour into this market in the coming years. Incumbents, cable companies, challenger telcos and non-telco entities like energy companies, municipalities and PE/infrastructure funds all have key roles to play in building sustainable nationwide gigabit fiber in their respective markets. Proactive moves from some Telcos like Vodafone DE or nontelcos like Open Fiber have placed them in a leading position in shaping the gigabit future of their markets. Incumbent telcos have made and are continuing to make big moves, as rumored in Italy and a few other European markets.

If we assume that the deal volume in 2020 will be approximately 60€ billion (similar to the volume in 2019) and assume a similar 40 percent of share of fiber or open access fiber in the total deal volume, we predict funding of 24€ billion going into the fiber sector in Europe. Assuming an average of 1000€ CAPEX required to pass a home with fiber, this implies 24 million new homes can be passed with fiber in 2020 alone. To put this in perspective, the whole of the UK or France can be passed with fiber in just one year. As availability of open access fiber increases, we will see a proliferation of multi-gigabit offers in the market delivered over FTTH, as we have already seen in Singapore and which are also occurring in Italy, Spain and Portugal, among others.

We will continue to watch with interest and report on the developments in this space in the future.

DOWNLOAD THE FULL REPORT

RELATED INFORMATION

Arthur D. Little: Decisive National Fiber strategies needed to boost future economic growth

The telecom industry, governments and regulators need to move decisively to fiber in order to support future economic growth, states Arthur D. Little (ADL) in its new report, “National Fiber…